Quest: Listing on the Warsaw Stock Exchange

The game development market in Poland and worldwide is steadily growing, and ambitious companies from the game sector are looking for ways to increase brand recognition and raise funds for new productions. This leads them to consider listing their shares on the stock exchange. So the question is, who can go public, what is to be gained from doing so, and how to go about it?

An IPO—is it right for us?

The basic question is whether a stock market listing is the best option. The answer depends on many factors and can vary depending on the candidate. But it is worth considering what benefits a company can gain by deciding to conduct an initial public offering.

The primary benefit is to raise capital for further development. If a company conducts an issue of new shares together with its debut on the stock exchange, the funds from the issue may be used for its current needs and planned investments. Often, the proceeds raised from investors allow the issuer to implement large business projects that would otherwise remain unrealised. Unlike bank financing, financing through a public issue is not based mainly on the financial results to date and the current financial condition of the company, but is largely dependent on the assessment of its chances for further growth. Therefore, this form of raising capital can also be used by entities that would find it difficult to obtain bank financing.

Going public also opens the way to raising capital from investors in the future through further share issues by a company already known to the market.

Another advantage of going public is increased prestige and brand recognition. Generally speaking, companies listed on the stock exchange are perceived by the market as reliable and stable entities, due to the additional requirements imposed on them and the rules they have to observe. In Poland, a listing on the Warsaw Stock Exchange proves to the market that the company is a mature organisation. So listing the company is a form of additional promotion.

Becoming a public company also brings benefits for shareholders. If they want to cash out some or all of their shares, an IPO may involve a sale of shares by existing shareholders. On the other hand, if they stay with the company, the effect of the IPO can increase the value of the shares and their liquidity for the future.

Team up

The key to a successful IPO is the selection of experienced advisers to help build a consistent and credible image of the company that will be persuasive for investors. A public offering and stock market debut are the result of a long and complex process requiring proper preparation in legal, financial and business terms. However, if the company chooses the right associates, everything can go smoothly.

The key players supporting the offering and listing are the legal adviser, the offeror, the auditor, and a public relations and investor relations (PR/IR) adviser.

-

Legal adviser

To conduct an IPO, the company will need to retain a team of lawyers specialising in capital markets law, in particular advising on public offerings and listing of companies.

Also, the nature of game development companies’ operations requires the participation of specialists in other fields of law, such as intellectual property, employment, state aid or regulatory law, whose involvement in the process will help smoothly resolve any potential problematic issues that need to be presented in the prospectus. Since game development companies typically operate in the international arena, it is worth finding an experienced law firm working with entities and laws of other jurisdictions to approach the foreign aspects of the company’s activity with understanding.

In the IPO process, the legal adviser most often coordinates preparation of the offering documentation and work on the prospectus, including:

- Performing due diligence on the company for matters required to be disclosed and described in the prospectus

- Preparing the company for market entry in terms of corporate governance and compliance

- Preparing and coordinating work on the prospectus

- Representing the company in proceedings before the Polish Financial Supervision Authority (KNF) and coordinating the process of approval of the prospectus by KNF.

If the company going public on the WSE is in the form of a limited-liability company (sp. z o.o.), it needs to be converted into a joint-stock company (SA) before the actual IPO process can take place. The legal adviser also handles this.

-

Offeror

Only an investment company can serve as the offeror. In practice, companies usually entrust this function to a brokerage house. Along with the legal adviser, the offeror is the key entity leading the IPO, and from the very beginning of the process its involvement is essential.

The brokerage is responsible for the business preparation of the company for the offering. Even before working on the prospectus, the offeror analyses the company from an operational point of view, proposes a strategy for carrying out the offering, and helps choose the best time for an IPO and determine the parameters of the offering. In subsequent stages, the brokerage not only intensively participates in drafting the prospectus, but also coordinates the offering process and supports the company in proceedings before KNF, the Warsaw Stock Exchange, and the Central Securities Depository of Poland (KDPW).

Often the offeror also acts as the manager of the offering—necessary to direct the share offering to institutional investors. The manager organises meetings with investors before the start of the transaction (“early-look” meetings, “pilot fishing,” roadshow), coordinates the selection of institutional investors, and is responsible for building the demand book and setting the final price for the shares.

-

Auditor

The function of the auditor within the public offering is performed by a chartered accountant as an entity authorised to examine the financial statements.

The auditor prepares the company for its stock exchange debut from the financial side, compiles the financial data, and audits historical data prepared for the prospectus. If a company reports using Polish accounting standards, the auditor can also assist the company in the transition to international standards (IFRS/IAS).

-

Public relations and investor relations

It is also worthwhile to establish cooperation with a PR agency to plan the company’s communications with the market throughout the process. The agency oversees the marketing message related to the IPO and controls the company’s communications with the media.

Go pro, or how to do it

Once the advisory team is assembled, the company can begin the actual IPO process.

-

Conversion (possibly)

If the company has the form of a limited-liability company, the first step is to convert it into a joint-stock company. Importantly, the transformation process is not an obstacle on the way to the Warsaw Stock Exchange. On the contrary, if the transformation into a joint-stock company is properly combined with the due diligence process, the legal adviser can help avoid the often tedious adjustment of the company’s corporate structure to the requirements of the WSE.

-

Due diligence

The next stage is the company’s due diligence, where advisers analyse the issuer from a legal, operational and financial perspective, identifying information that needs to be disclosed in the prospectus to enable investors to make an informed investment decision. Due diligence helps ensure that data in the prospectus are true, fair, complete and accurate.

One of the key elements of due diligence is identifying risk factors associated with the company’s operations. The risk factors are a mandatory element of the prospectus and allow investors to assess whether they can accept the level of risk associated with the activities of the company.

In principle, due diligence includes an examination of the company’s legal status, capital group, organisational structure, corporate issues, employee issues, and the company’s relationship with its counterparties. Depending on the type of activity undertaken by the company, due diligence may also include specific legal issues requiring additional expertise, such as intellectual property law, environmental law, regulatory law, or public law if the company benefits from grants or subsidies.

As part of the due diligence process, the legal adviser also helps the company adopt corporate governance principles typical for public companies. This includes amending the company’s articles of association and bylaws, appointing an audit committee, and preparing additional internal regulations.

Corporate preparation of the company also includes drafting and adoption of resolutions of the general meeting necessary for listing on the WSE: a resolution on the issue of new shares, which will be covered by the prospectus, and a resolution on applying for admission of shares covered by the prospectus to trading on the regulated market.

A public company should also observe the Code of Best Practice for WSE Listed Companies. It is not compulsory to follow all practices, but the company has to account for not following them. Therefore, it is crucial for the company, in consultation with its legal adviser, to select the practices it will follow and make a good case for not following others, in accordance with the “comply or explain” principle.

-

Prospectus

The prospectus is the basic document presenting the company and the contemplated offering. It contains information investors need to make an informed assessment of the company.

The substantive scope of the prospectus, as well as the method of presenting the information, is governed by the EU’s Prospectus Regulation (2017/1129) and the Act on Public Offerings of Financial Instruments. The information contained in the prospectus must be written and presented in a concise, understandable and easy to analyse form.

Usually, preparation of the prospectus is coordinated by the legal adviser, which also drafts the legal part of the document. However, all advisers and the company itself are involved in drafting the prospectus. As the key document in the offering, the prospectus must reliably and completely present the legal status of the company, its business model and market position, as well as fulfil a marketing function and encourage investors to purchase the company’s shares. The involvement of all parties is essential to ensure that all parts of the prospectus complement each other and form a readable and accessible whole for investors.

The prospectus is submitted to KNF for approval. During the proceedings, KNF verifies the prospectus for its completeness, comprehensibility and consistency, and approves it once the company and the advisers have addressed all comments and additional requests made by KNF.

The procedure before KNF ends with a decision approving the prospectus, as the culmination of the administrative process. The company or the offeror will then publish the prospectus on its website immediately after approval.

-

Offering

The actual offering is coordinated by the brokerage and includes several key events targeted to different classes of investors.

Relations with institutional investors are established during roadshows and book-building.

Roadshows are meetings of the company’s managers with potential institutional investors, organised by the brokerage. Their purpose is to present the company to investors and encourage them to take part in the offering.

As part of book-building, the brokerage sounds out the interest of institutional investors in the company’s share offering. Based on the conclusions from this process, the company and the brokerage determine the final terms of the issue, i.e. the price and number of shares to be sold.

The brokerage also directs the offering to individual investors, who can place subscriptions for shares under the rules set forth in the prospectus.

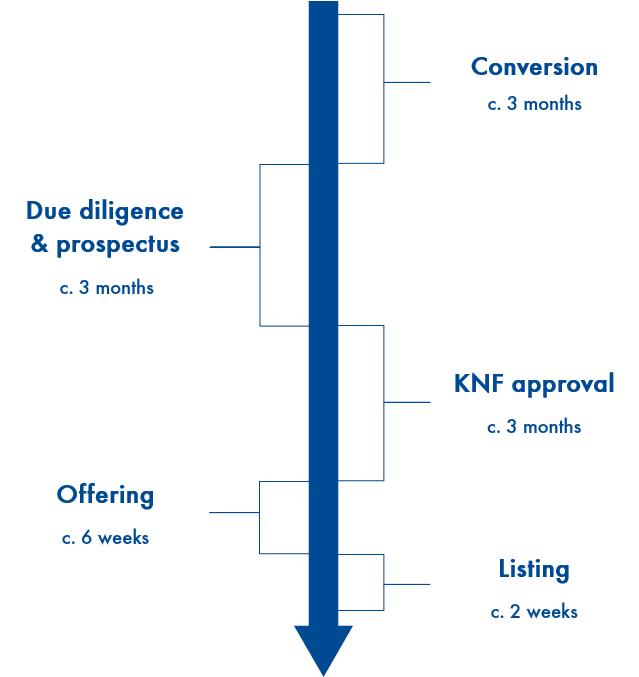

How long does it take?

One of the main questions companies ask at the beginning of an IPO is how long the entire process will take. But this is one of the most difficult questions to answer, and the best answer is “it depends.” It depends on…

…the internal organisation

For the legal examination to begin, the company must provide a range of information and documents. Depending on the level of organisation in the company, gathering all the data can take a few days to several weeks.

…the type of business

The legal and operational analysis of the company is a key part of preparation of the prospectus. The duration of the analysis depends largely on the complexity of the company’s organisation and its business. As a rule, with active participation of the company and advisers, the due diligence process should take about two months.

In the course of due diligence, the legal adviser begins to draft the prospectus. As the prospectus is based on the results of the legal and operational analysis, the time it takes to draft the prospectus depends on these results. The prospectus should present the company as fully as possible. This helps expedite the explanatory proceedings before KNF. Again, with active participation of the company and all advisers in completing the prospectus, work on the document should take around three months.

…the regulator

The prospectus is subject to approval by the Polish Financial Supervision Authority. First, KNF engages in an investigation, submitting comments to the prospectus, which should then be addressed by revising the prospectus or otherwise clarified. In practice, the process of approval of the prospectus takes two to three months, but sometimes it can last much longer.

…business decisions

The timing of the offering and subscription of shares is a business decision agreed upon at the beginning of the process by the brokerage and the company.

…WSE and KDPW

To carry out the listing, together with its advisers, the company must also apply to register the shares and admit the shares to trading on the regulated market. The Central Securities Depository of Poland (KDPW) registers the shares after adopting a relevant resolution. Before considering the application for admission of the shares, the WSE analyses the prospectus and the terms of the offering, and if the company satisfies all the conditions set forth in the law and the WSE rules, adopts a resolution to admit the shares to exchange trading and then a resolution to list the shares and set the first trading day.

Good luck and have fun

So, who can be listed on the stock exchange? Any company serious about growing its business and strengthening its position on the market.

First and foremost, the company benefits from listing on the WSE by joining the group of major players aspiring to become the largest entities on the market, consistently gaining the trust of investors. The positive consequences for the shareholders resulting from a company going public are also significant.

Above, we briefly present the path to a successful debut on the WSE. Although the IPO process is complex, it can be implemented smoothly. With the help of experienced advisers, the road to become a stock market bull may prove easier than it seems. So good luck and have fun.

Katarzyna Jaroszyńska, attorney-at-law, Marcin Pietkiewicz, attorney-at-law, Capital Markets & Financial Institutions practice, Wardyński & Partners